When the Mag7 Bend the Factor Space

The Magnificent 7 haven’t just reshaped U.S. indices - they’ve reshaped factors.

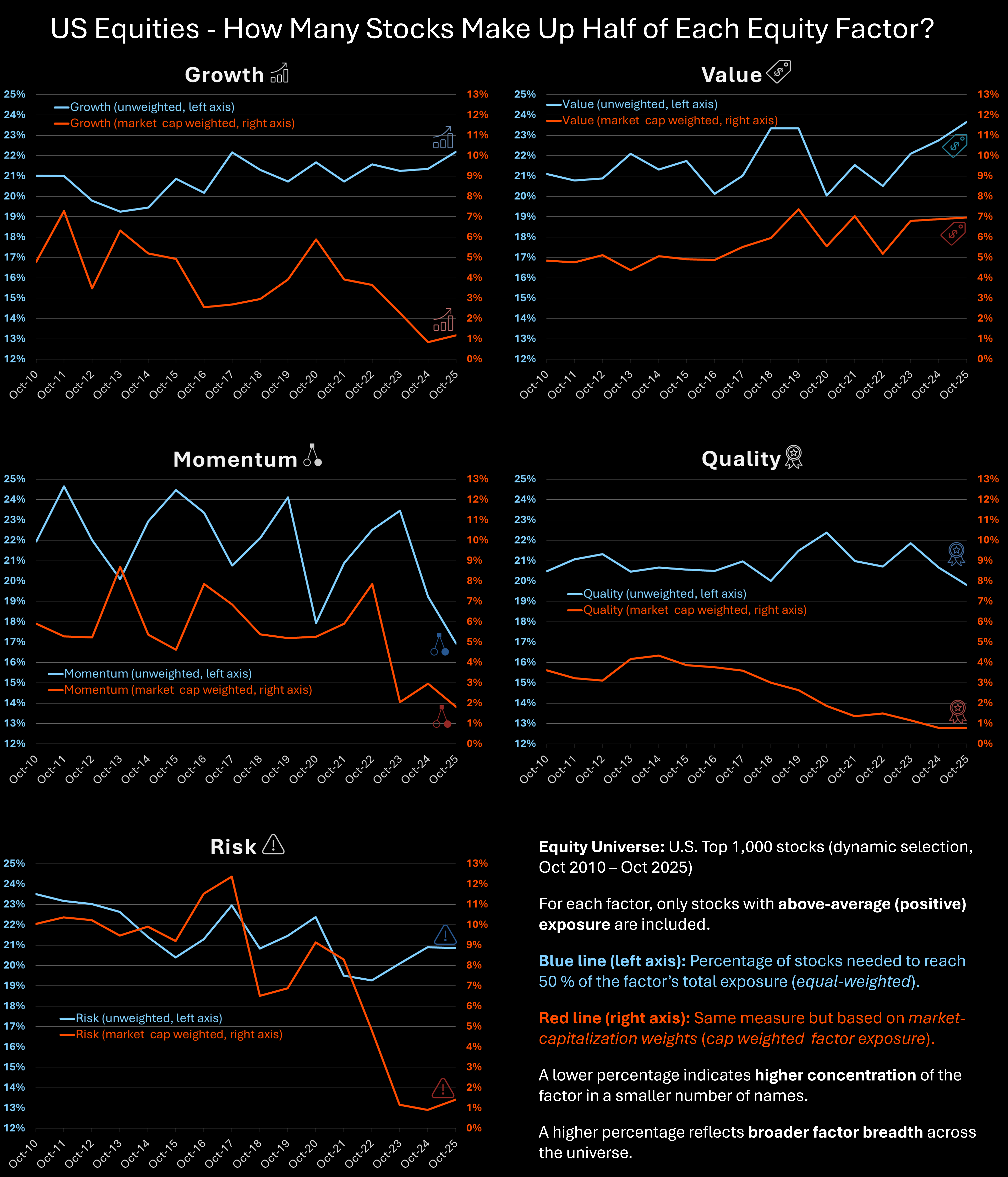

Using Sismo’s factor analytics on the largest 1 000 U.S. stocks (Oct 2010 – Oct2025), we examined five equity styles - Growth, Value, Momentum, Quality and Risk.

For each factor, we focused on stocks with above-average exposure and measured how many account for half of the factor’s total exposure once weighted by market capitalization.

Each chart shows this percentage over time:

Blue = unweighted (% of stocks)

Red = market-cap weighted (% of stocks)

What we found

In 2010, most factors were broad: 15 – 50 stocks were needed to reach 50 % of total exposure.

By 2025, four - Growth, Momentum, Quality and Risk - had become much narrower, dominated by the same mega-caps

The overlap is striking: the same small group sits at the intersection of multiple factors.

Their extraordinary rise has tilted the factor space itself, creating a multi-factor concentration unique in modern U.S. equity history.

Interpreting the picture

The blue lines have remained relatively stable.

This shows that factor structures themselves persist - there are still growth, value and quality stocks.

For stock selection, factor analysis remains a valid and powerful framework.

The red lines, however, reveal how market-cap dynamics - accelerated by the AI revolution - have concentrated the economic weight of several factors into a handful of names.

What changed is not the existence of factors, but their representation in today’s market.

Why it matters

Diversification across styles works only if their drivers remain distinct.

But when the same names dominate several factors, portfolio risk becomes less diversified than it appears.

A shock to a single company - say Nvidia - can ripple through Growth, Momentum, Quality and Risk exposures.

Research calls this factor crowding or narrow breadth:

The market still looks diversified.

The risk isn’t.