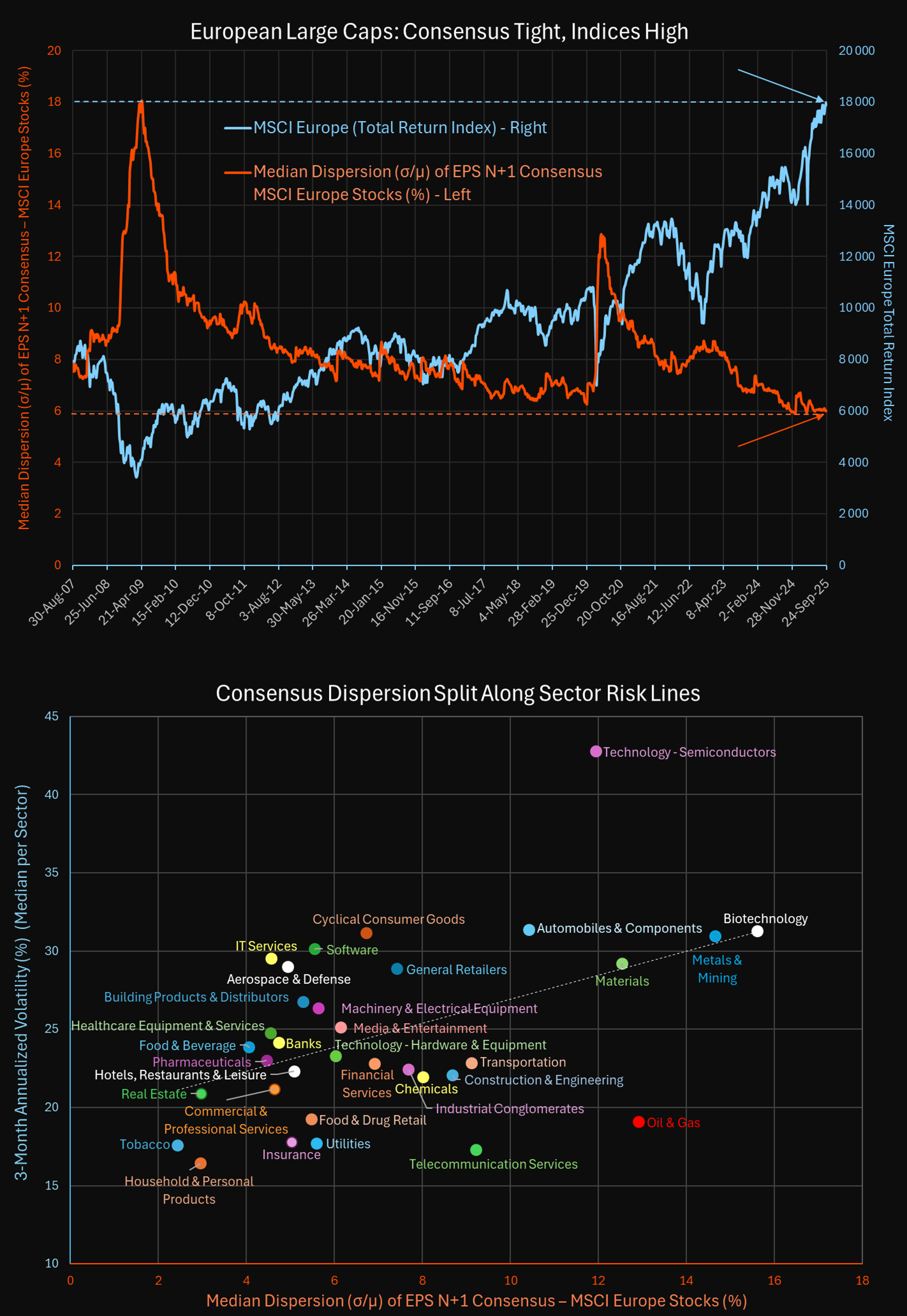

On European large caps (MSCI Europe), the median dispersion of broker forecasts on EPS N+1(σ/μ) has fallen to a record low of ~6%. At the same time, the index is at record highs.

Analysts have never agreed more on next year’s earnings, even while Europe faces:

- War on its doorstep: Russia’s war in Ukraine drags into its fourth year, keeping energy security fragile and defense spending elevated.

- Ballooning public deficits: France (~–5.8% of GDP), Poland (~–6.6%), and Slovakia remain far above the EU’s ceiling. Debt/GDP ratios are also elevated - 114% in France, 138% in Italy, 152% in Greece - leaving little fiscal room to maneuver.

- Rising trade frictions with the US: Escalating tariff disputes over green tech, autos, and subsidies, while the Inflation Reduction Act tilts competitiveness away from European producers.

- Near-recession conditions: Growth has stagnated. The euro area barely expanded in 2024, with Germany in technical recession and PMIs still flashing weak demand. The ECB’s tighter policy and high real rates weigh on investment.

How can forecasts look so “predictable” when the environment is so uncertain?

When low dispersion hides risk

In Hide in the Herd: Macroeconomic Uncertainty and Analyst Forecast Dispersion (Chen, Zhao & Zhou, 2025), the authors show that:

- Dispersion falls when macro uncertainty rises - the opposite of what intuition might suggest.

- Analysts herd more aggressively under uncertainty, clustering around the same numbers.

- Firms with stronger herding show less informative prices relative to fundamentals and lower subsequent returns in the cross-section.

So tight consensus may reflect conformity, not clarity.

Academic view vs Sismo back-test

- Academic evidence (Chen, Zhao & Zhou, 2025): low dispersion under uncertainty often reflects herding and is associated with less informative prices and weaker subsequent returns in the cross-section.

- Sismo back-tests (MSCI Europe, 2009–2024): over 15 years, portfolios tilted to high-dispersion stocks have generally shown an advantage versus low-dispersion portfolios. But regime matters: in certain periods - for example, in the first six months following the Covid outbreak - low-dispersion stocks outperformed, largely because they clustered in defensive, low-volatility sectors that investors favored during the shock.

In other words: there is no contradiction - dispersion sorts appear to capture a blend of volatility and sector bias, with the relative advantage of high vs low dispersion depending on the market environment and risk appetite cycle.

Takeaway

Low dispersion today doesn’t mean next year’s earnings are genuinely predictable. It may simply mean analysts are reluctant to deviate.

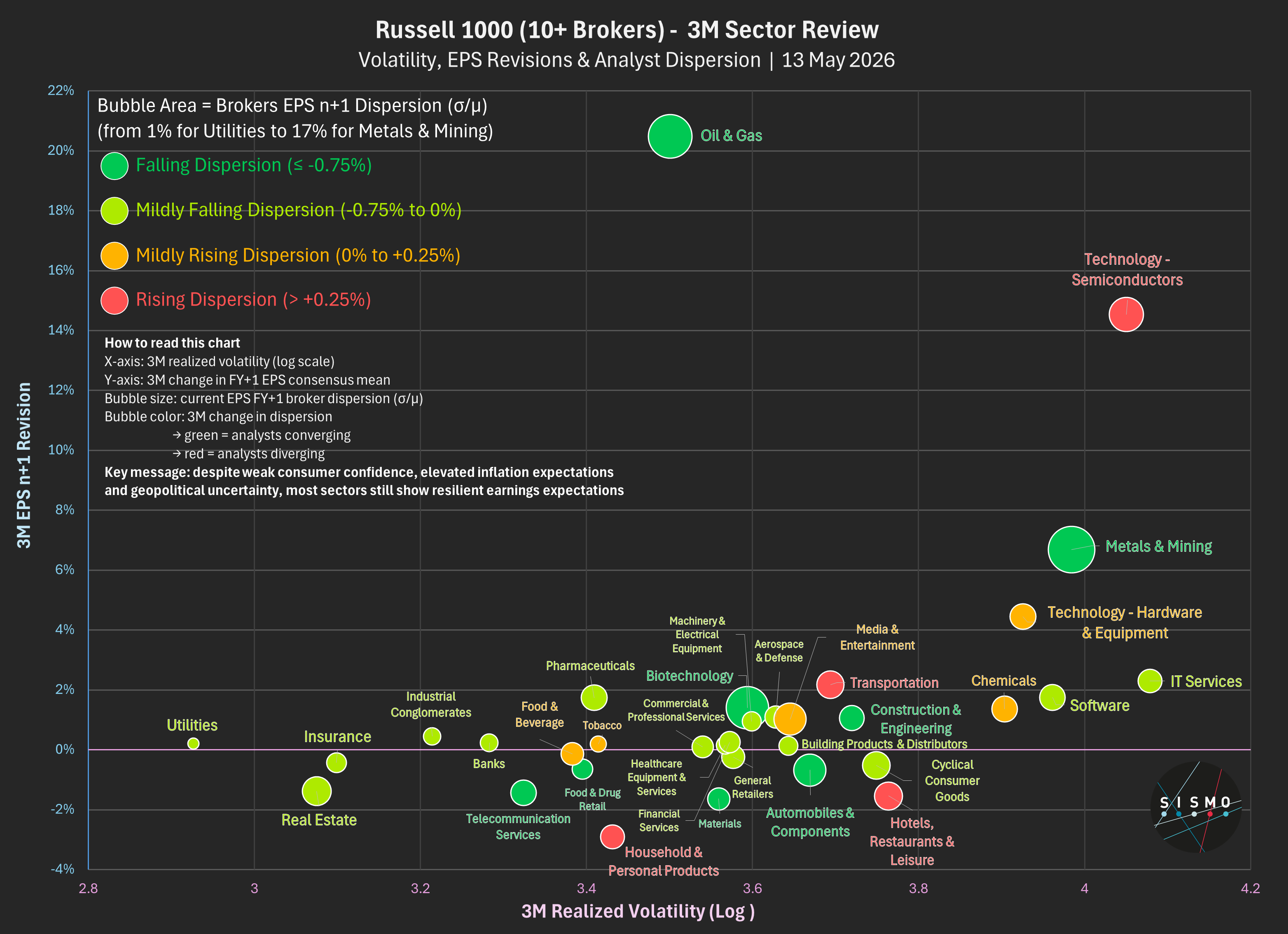

For investors, the real signal lies in the cross-section: even when the overall median is tight, sector gaps in dispersion remain - and that’s where risks and opportunities arise.