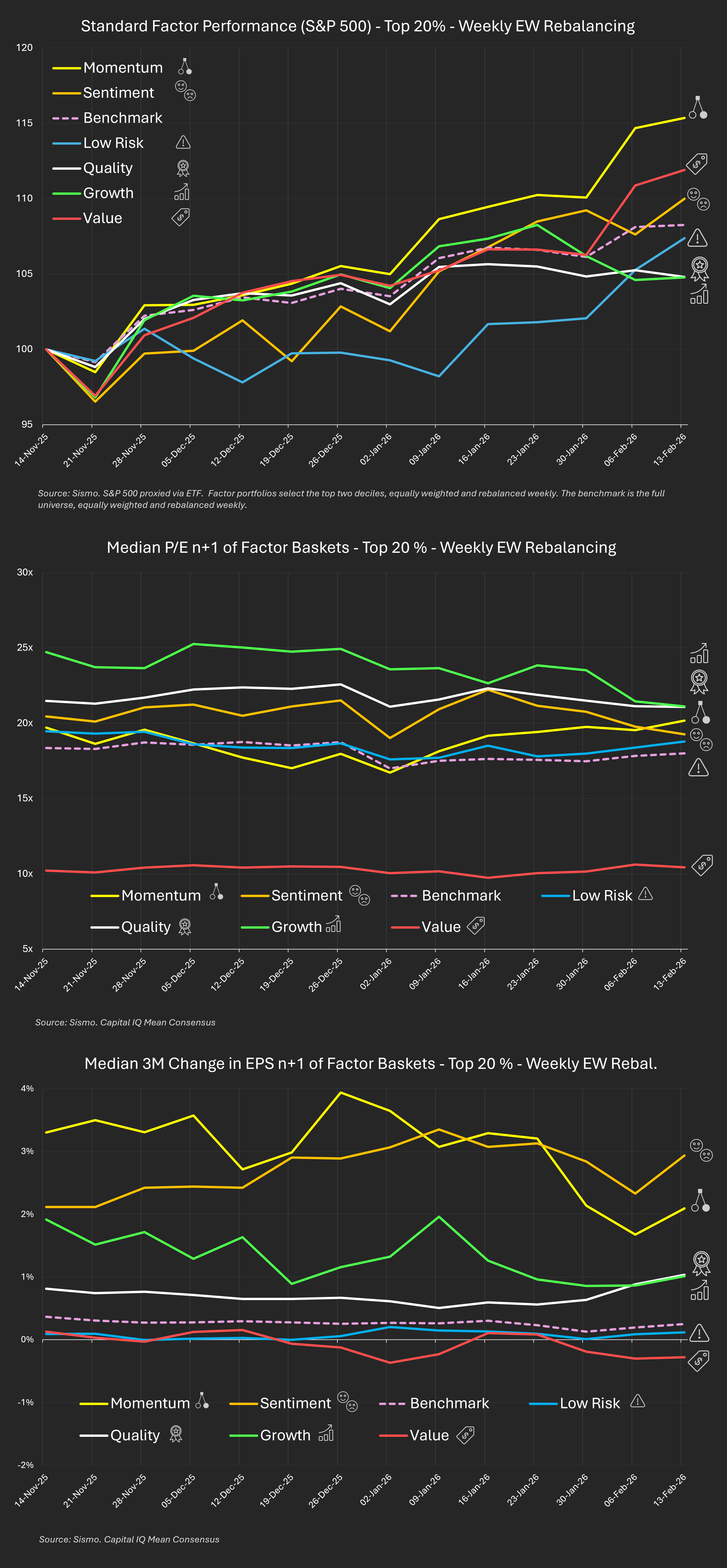

The last three months in the S&P 500 weren’t random.

The divergence across styles tells a clear story.

Using weekly rebalanced top-20% factor baskets, measured against the full equal-weight universe, here’s what happened:

Mid-Nov → Mid-Feb

- Momentum: +15%

- Value: +12%

- Equal-weight universe: +8%

- Growth & Quality: ~+5%

Dispersion widened materially - especially from early January, during earnings season.

Returns alone don't explain much.

So we decomposed the drivers.

For each basket, weekly, we tracked:

- Median FY+1 P/E

- Median 3M change in FY+1 EPS estimates

(valuation interpretation excludes the FY roll at year-end)

What drove the divergence?

Momentum: earnings-backed leadership

- Highest earnings revision profile (~3% vs ~0.3% for the universe).

- Modest multiple expansion.

- Leadership appears fundamentally supported.

Value: re-rating despite weak revisions

- Revisions flat to negative.

- Multiples expanded.

- Performance looks re-rating driven.

Growth & Quality: a de-rating phase

- Revisions positive but not accelerating.

- Multiples compressed.

- Underperformance appears valuation-driven.

The broader point

The last three months weren’t a simple “risk-on” phase.

They reflect:

- Earnings-backed leadership

- Valuation catch-up in discounted names

- De-rating in expensive segments

Different drivers. Same market.