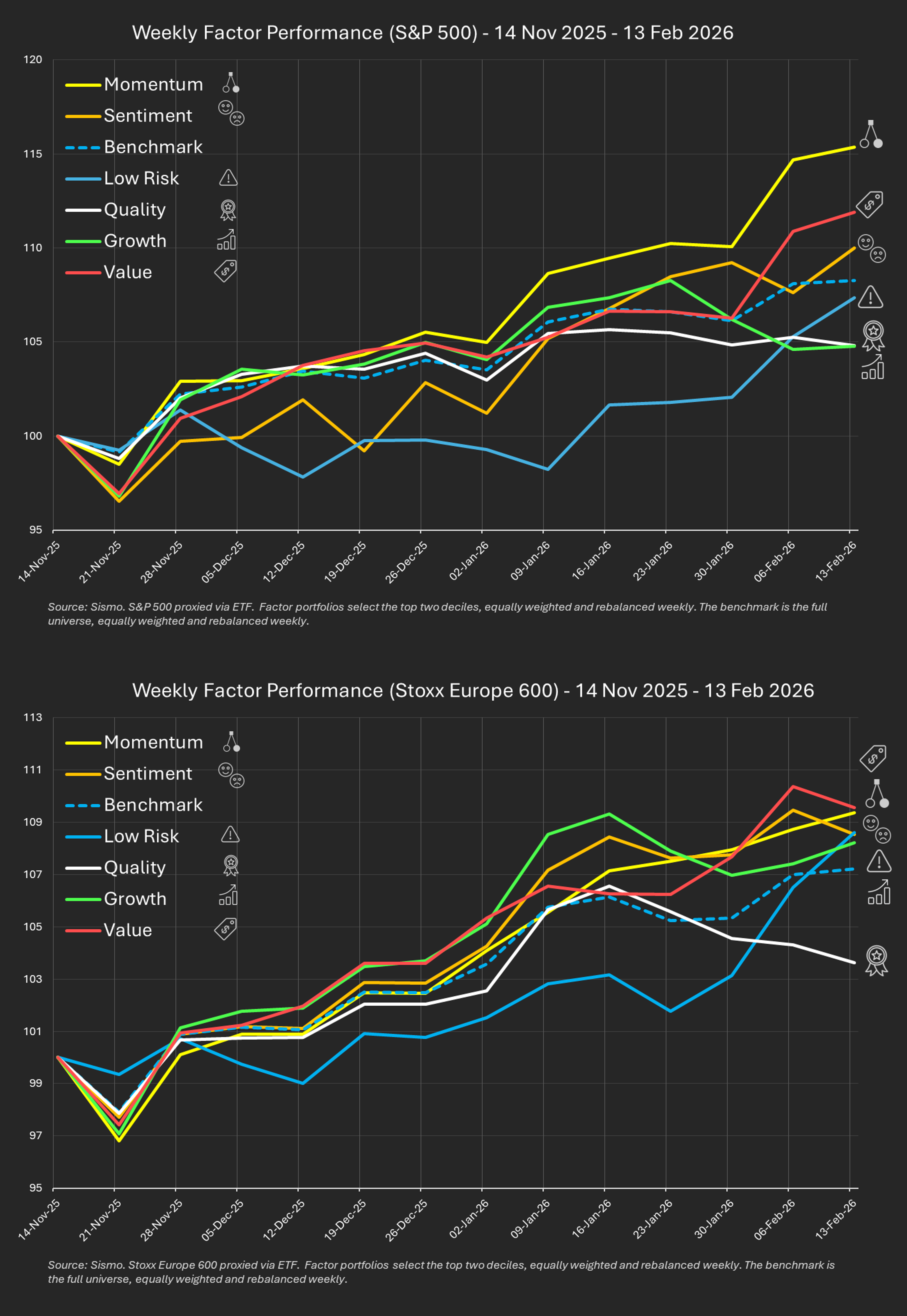

Since late December, relative factor leadership has strengthened rather than reversed.

We analysed weekly rebalanced top 20% factor baskets (equal-weighted) across:

Benchmarks are the full proxy universes themselves, also equal-weighted and weekly rebalanced.

This highlights relative performance across stocks - not index concentration effects.

Dispersion between factor leaders and laggards reached ~10 points.

The widening accelerated from early January - during earnings season.

There was no broad factor reset.

Relative trends strengthened.

Europe appears more balanced.

The US shows more concentrated leadership.

This period has been highly selective.

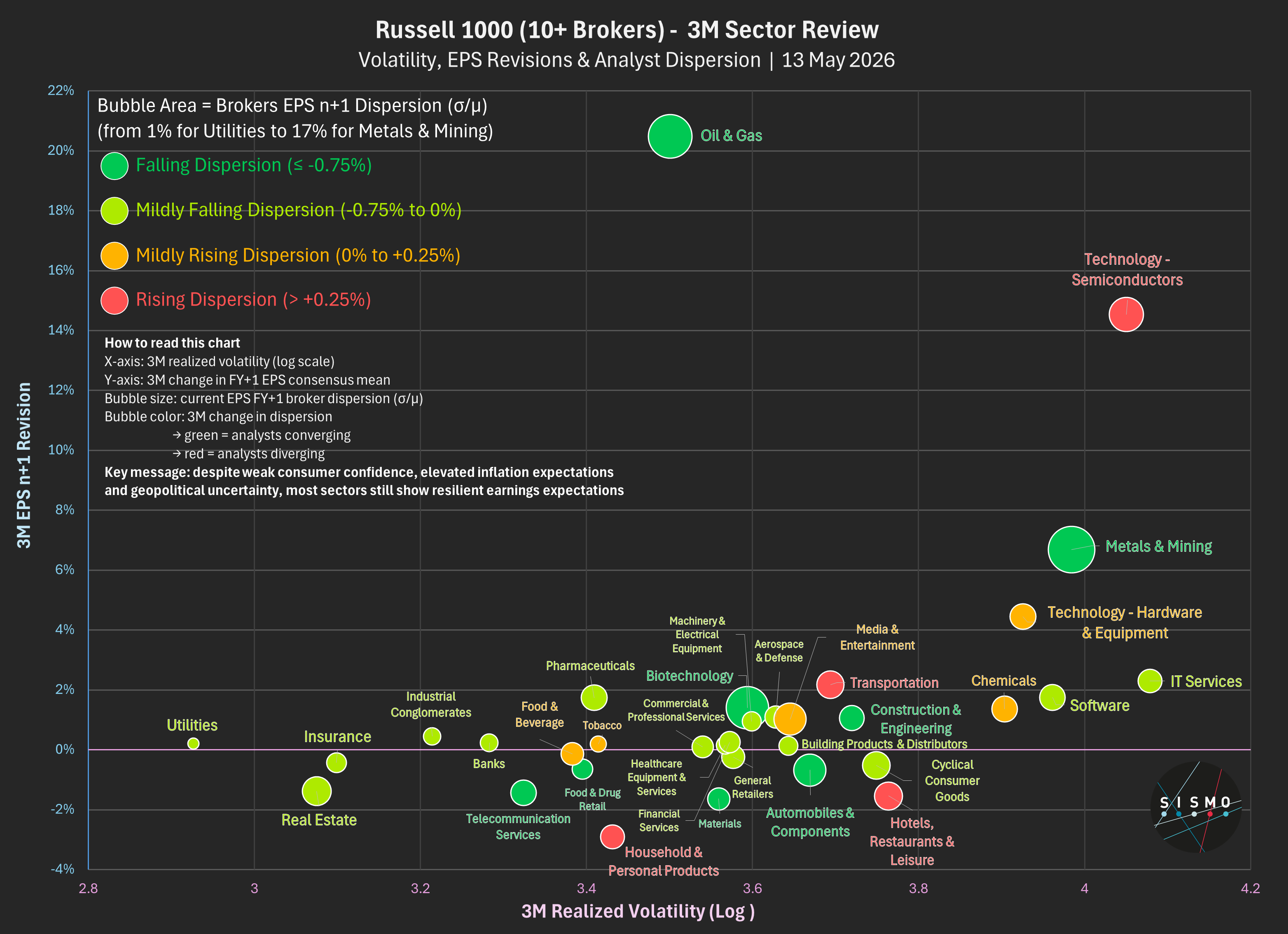

Certain industries - notably Software, repricing on AI-related competitive pressure - have been sharply penalised. Others have continued trending strongly.

At the factor level:

This does not look like a macro-driven regime shift.

It looks more like a reinforcement phase - where earnings season confirmed relative positioning rather than disrupting it.