That divergence may be one of the most important market signals today.

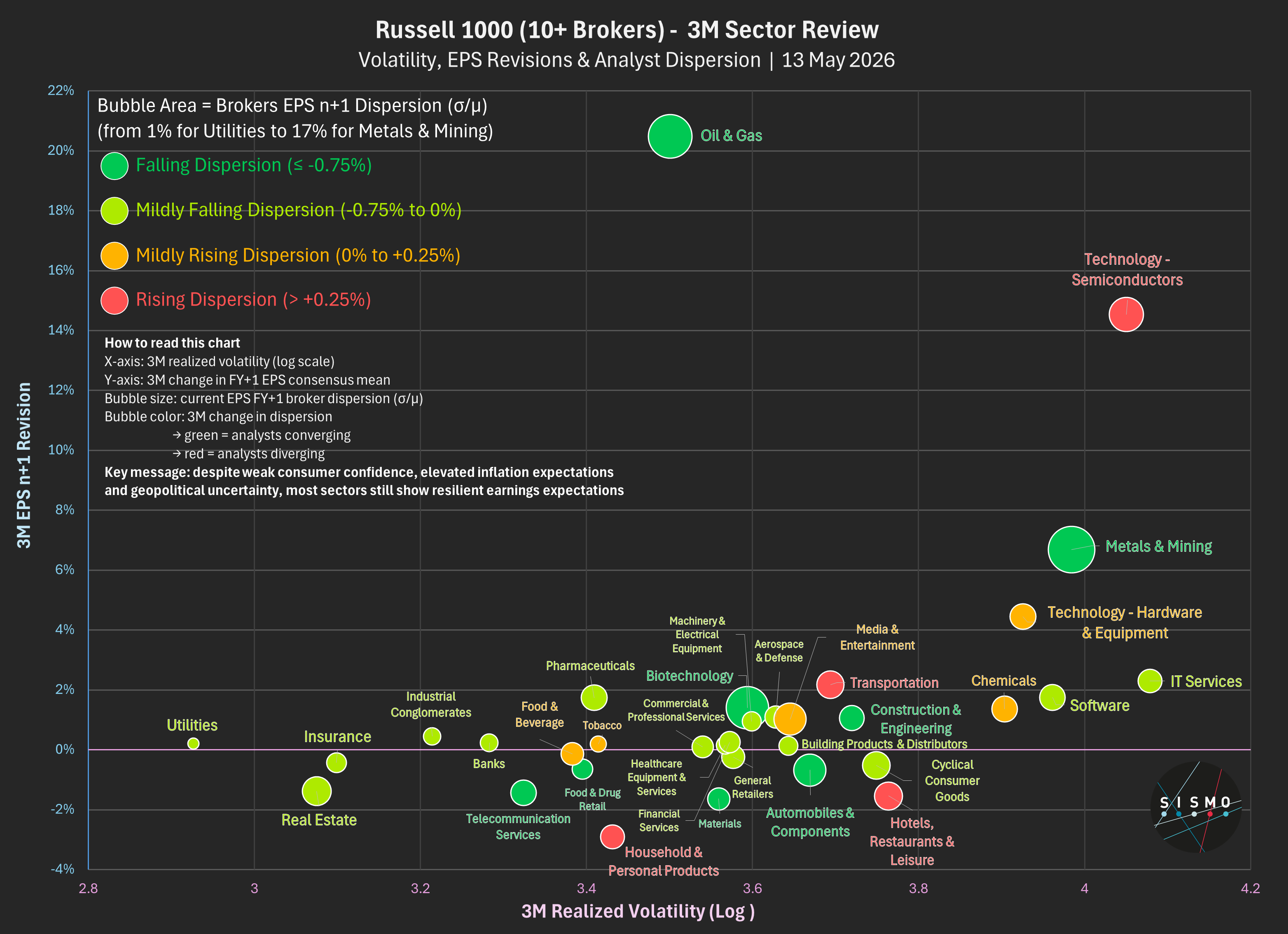

Using a Russell 1000 proxy filtered for stocks covered by at least 10 brokers (830 names across 33 Sismo sectors), we find that EPS revisions over the last 3 months remain broadly positive: the median FY+1 EPS revision across the universe stands at +0.45%.

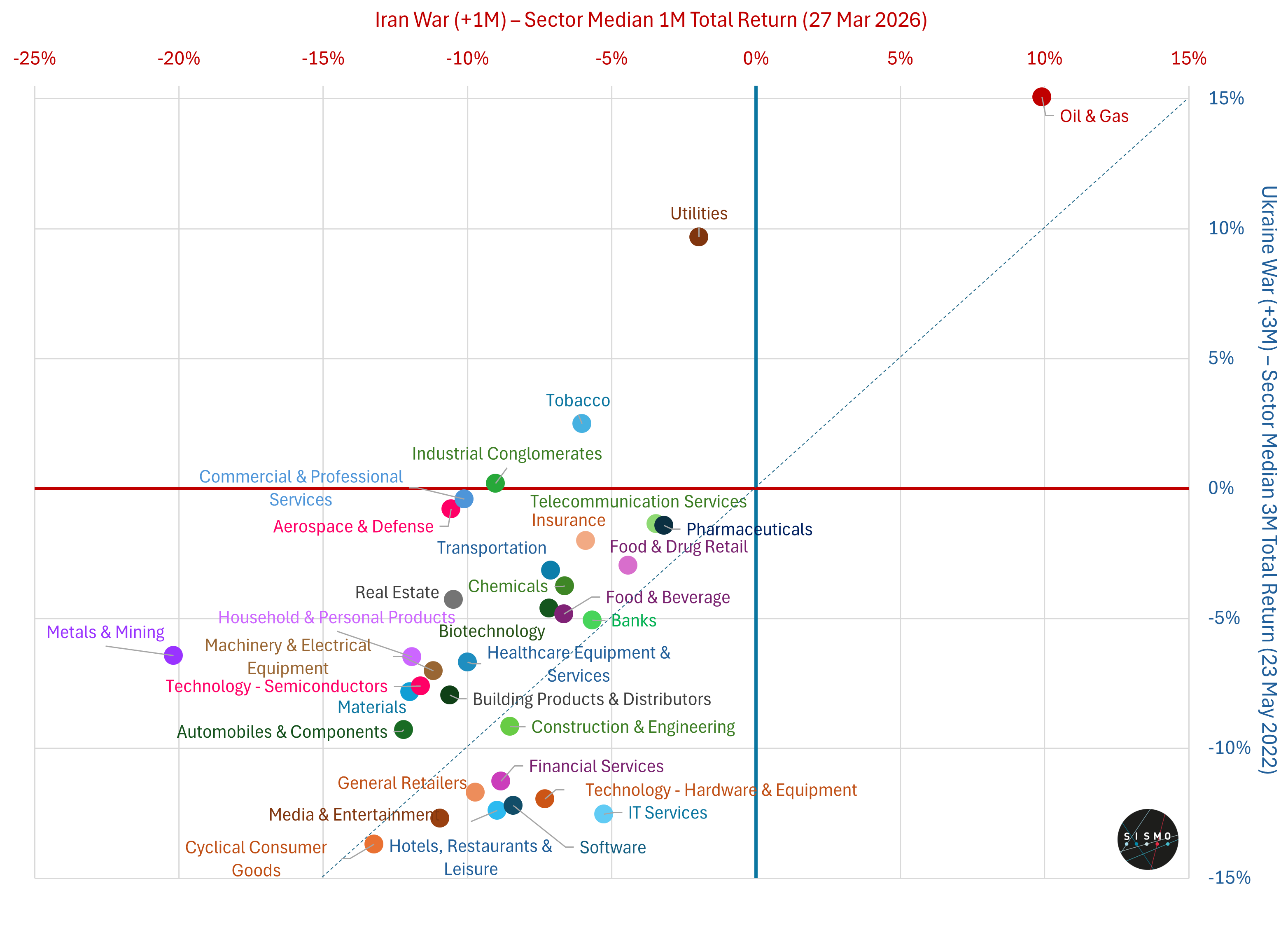

Despite geopolitical tensions - and nearly three months after the Iran conflict began - earnings expectations are improving, not deteriorating.

The strongest upward revisions are concentrated in:

• Oil & Gas

• Semiconductors

• Metals & Mining

• Hardware Tech

But the real signal comes from analyst dispersion.

Oil & Gas shows the strongest upward EPS revision (+20.5%), combined with high current dispersion but falling disagreement over the past three months. Direction is positive and analyst conviction has improved despite geopolitical sensitivity.

Semiconductors rank second for upward EPS revisions (+14.5%). Current broker dispersion remains moderate at 9.4%, but it has increased the most over the past three months (+0.7%). Analysts remain constructive on AI-driven earnings but the range of outcomes is widening.

Metals & Mining shows a similar but more uncertain pattern: strong positive revisions (+6.7%) combined with the highest current dispersion in the universe (17.4%), reflecting broad disagreement around commodity sensitivity and geopolitical outcomes.

Software and IT Services remain highly volatile, yet analyst disagreement is limited - as if consensus already agrees these sectors face structural pressure from AI.

Most surprisingly, broker dispersion has fallen across most sectors over the past three months.

In short:

geopolitical uncertainty ↑

earnings uncertainty ↓

At the same time:

• consumer sentiment is near historic lows,

• inflation expectations remain elevated,

• gasoline prices continue to rise.

Consumers are experiencing inflation in real time.

Equity markets continue to focus on earnings resilience.

Both cannot remain true forever.