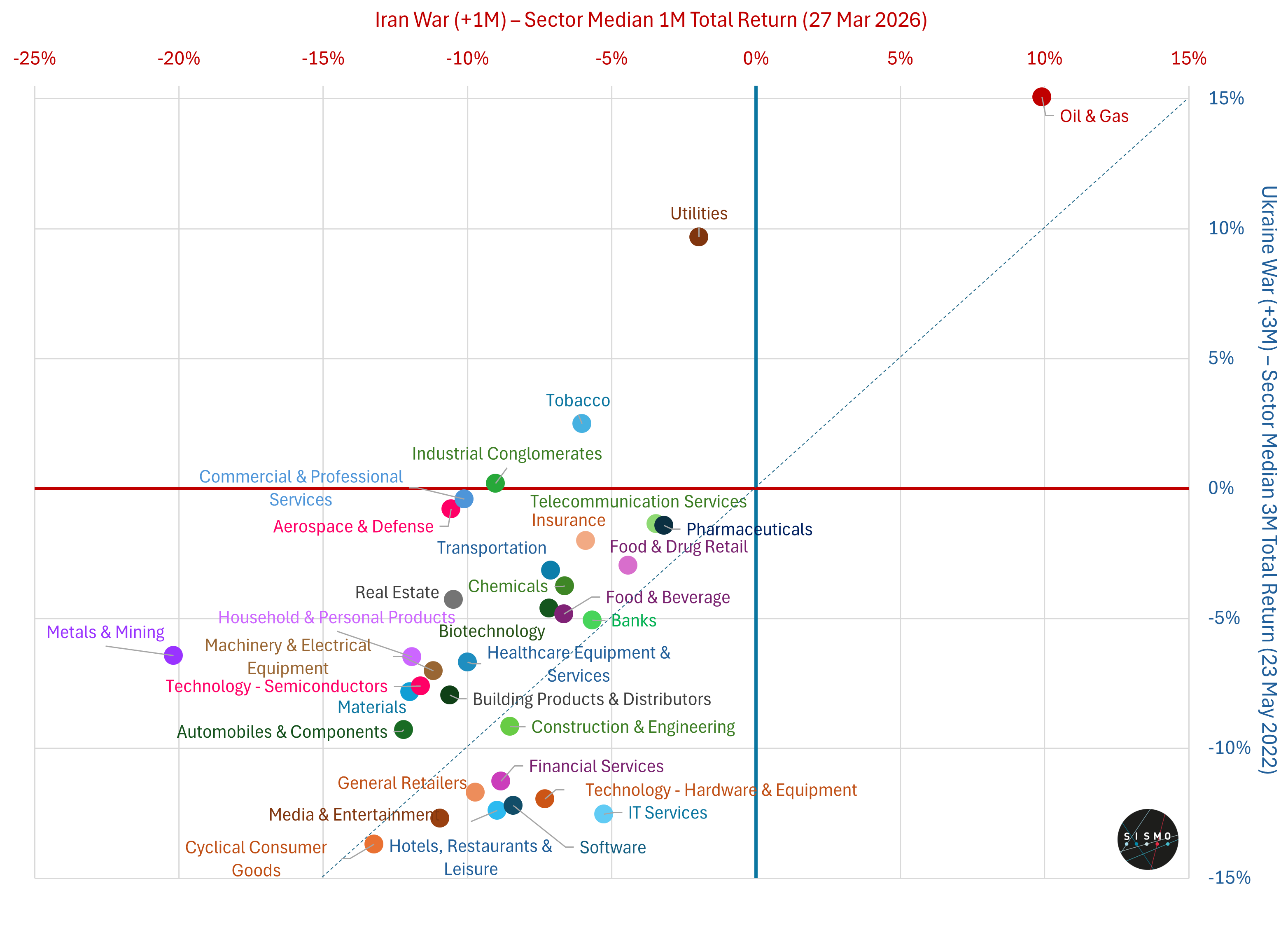

Using Sismo data (MSCI ACWI ETF proxy), comparing 1M after the Iran war (2026) vs 3M after the Ukraine war (2022):

The pattern is familiar but the magnitude and cross-sector signals are very different.

The shock is broader:

Median return is -8.25% after one month vs +0.69% (1M) and -5.73% (3M) in 2022.

The oil move is sharper:

Brent +45% in one month vs +16% over three months in 2022 - a faster, more disruptive shock.

In 2022, oil had already been rising for months (Dec 2021: $70 → $100 pre-war → $115 by May)

But the key difference is in sector behavior:

Metals & Mining -20% (vs -6%)

Utilities -2% (vs +10%)

Defense not outperforming

The data points in a different direction:

Energy is the only clear winner (+10%).

Economically sensitive sectors (Consumer, Industrials, Tech, Financials) are down between -7% and -14%.

Metals, a proxy for global industrial demand, is the worst performer.

Defensive segments are not providing upside: Utilities are negative and Defense is not outperforming.

Taken together, markets appear to be reacting not just to higher energy prices, but to the risk that rising costs and disrupted trade weigh on global activity.

Are markets already pricing a slowdown?