Earlier this week we showed how U.S. semiconductor companies rely heavily on Asia and China for sales. But that case is the exception rather than the rule.

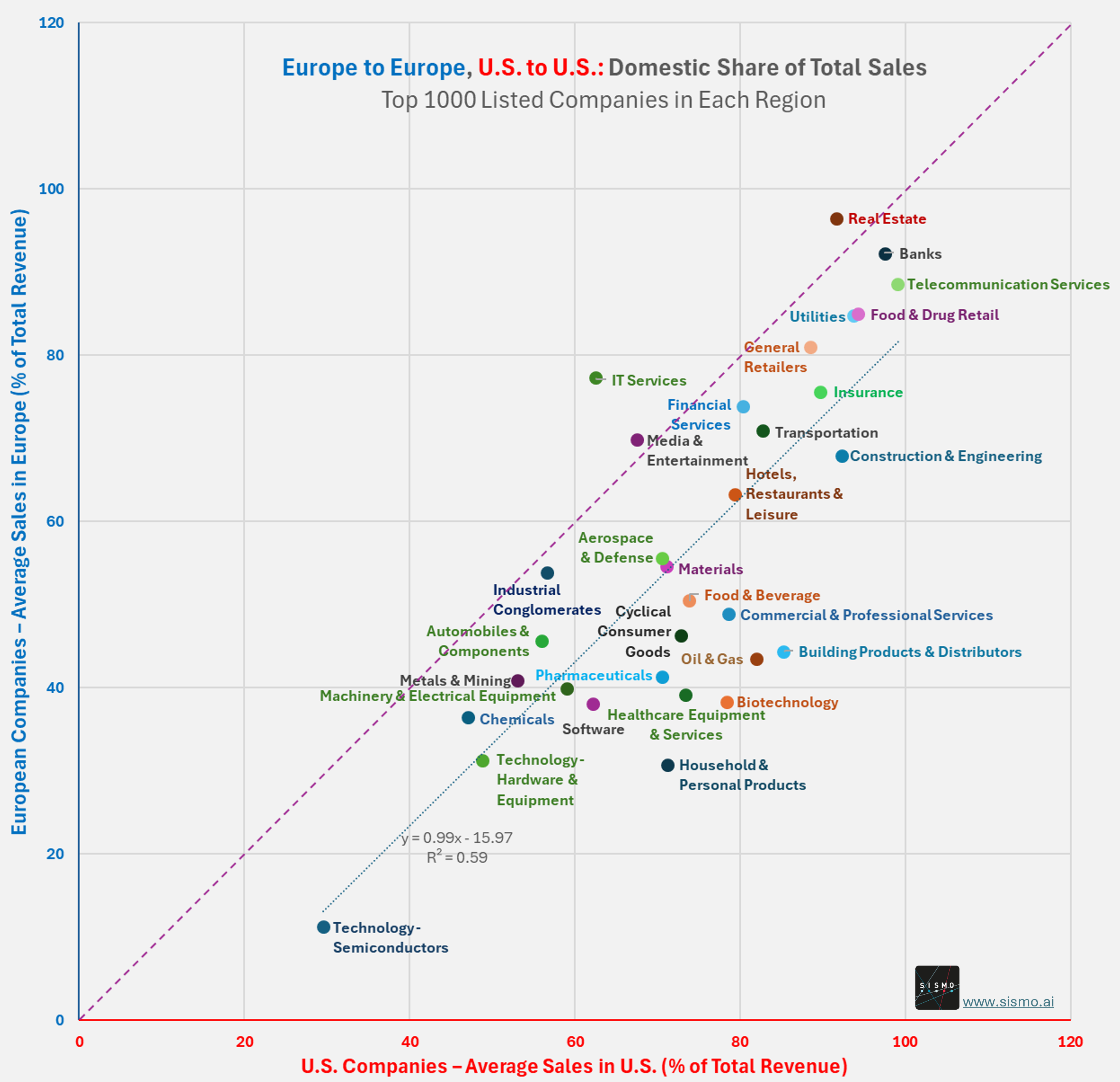

With Sismo, we looked at the top 1000 listed companies in the U.S. and in Europe and measured the share of sales achieved in their home markets.

The results are striking. On average, U.S. large caps earned 75% of their revenues domestically in 2024 (median 82%). European large caps earned only 61% domestically (median 63%). Out of 32 sectors, 29 fall below the parity line, meaning U.S. companies achieve a higher share of local sales in almost every industry.

Some examples illustrate the scale of the gap: U.S. biotech companies earned 78% of sales at home versus 38% for European peers; U.S. oil and gas companies 82% versus 43% in Europe; and U.S. building products and distributors 85% versus 44% in Europe.

The exception remains semiconductors. Here, U.S. companies generate only 30% of their sales domestically and European peers just 11%, underlining Asia and China’s dominant role in this sector.

The conclusion for investors is clear. For U.S. large caps, the domestic market is the primary driver. Whatever happens globally often matters only to the extent it affects U.S. economics. For European large caps, international markets are indispensable. Growth depends on them.