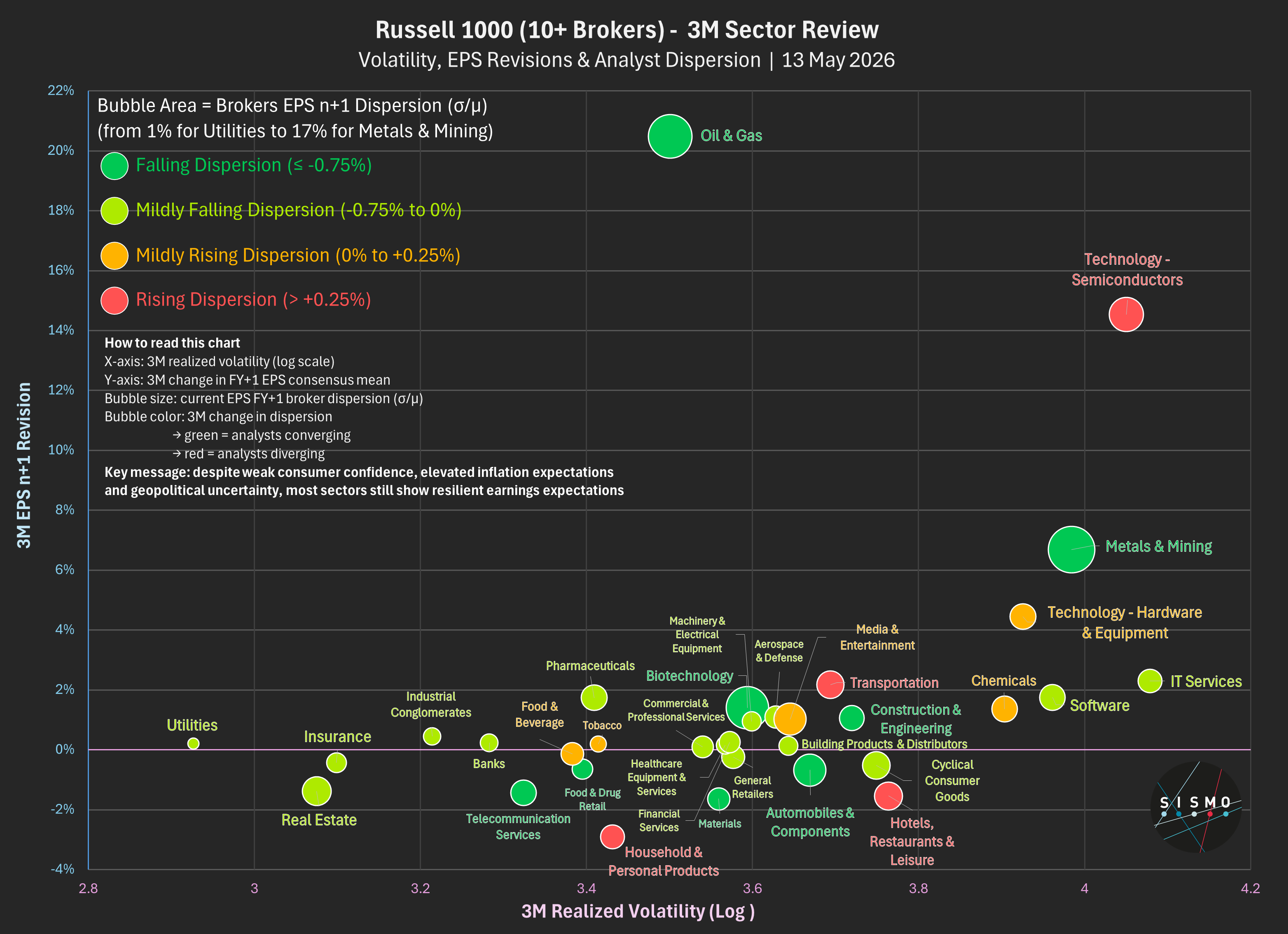

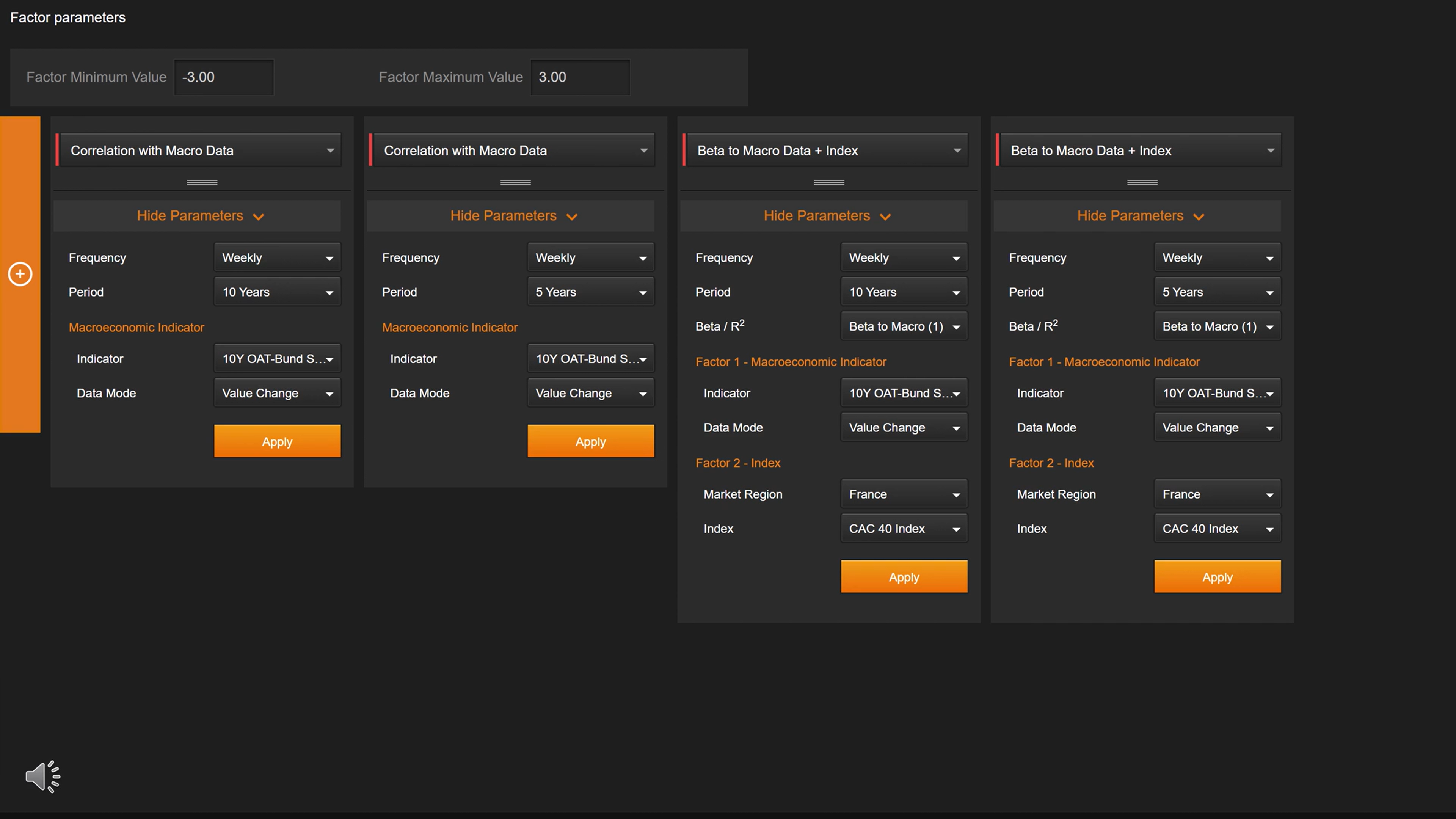

Following the surprise announcement of France’s snap elections, Sismo analyzed the correlation and beta of French stocks relative to the spread between the volatile French OAT and the German 10-year Bund. This revealed how political uncertainty and widening sovereign spreads connect to individual stock movements, giving portfolio managers a risk-aware view of market reactions.

Highlights:

Why It Matters:

Political shocks can trigger sudden spread movements that ripple through equity markets. By quantifying correlations and betas to sovereign spreads, investors can anticipate potential drawdowns, rebalance sector exposures, and mitigate political risk in equity portfolios.