Inspired by a recent FT article by Ruchir Sharma (“The best time to buy quality stocks is now”), we tried to test a simple idea:

have high-quality stocks really been neglected?

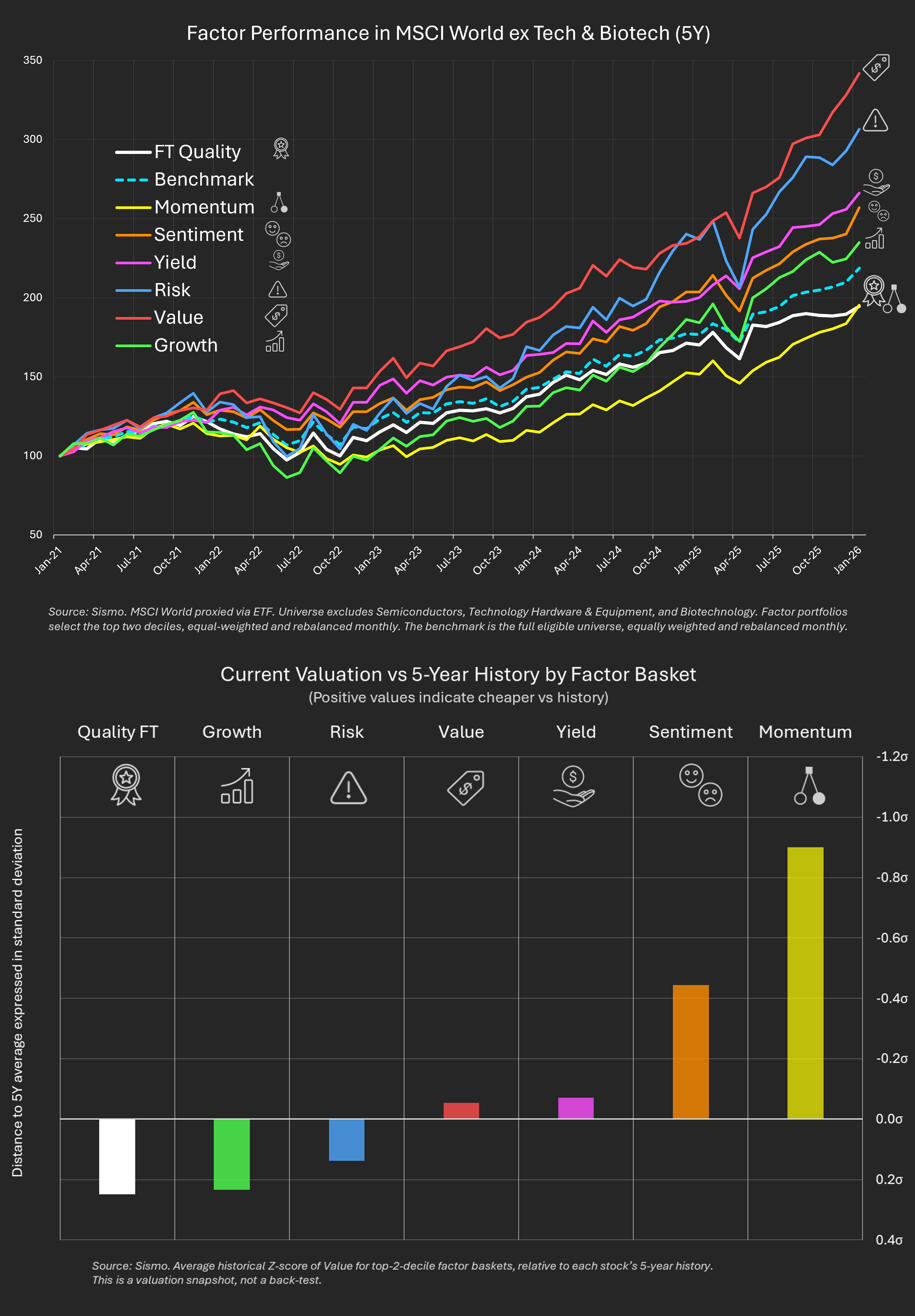

We built a Quality FT factor combining profitability, balance-sheet discipline and earnings regularity, and applied it to MSCI World excluding semiconductors, tech hardware and biotech - away from the front line of the AI narrative.

The back-test result is straightforward (top chart): quality has lagged over the past five years.

That’s not a bug. It’s the regime.

Markets rewarded:

As a result, non-tech quality stocks saw declining relative demand and compressed valuations - not because they were bad businesses, but because they didn’t match what the market was rewarding.

Looking at valuations today (not performance), the picture changes.

Relative to their own 5-year history (bottom chart), top-two-decile factor baskets show where their current valuations stand:

This setup doesn’t rely on timing the end of any narrative.

It simply reflects a growing gap between business quality and market attention.

And that gap rarely persists forever.