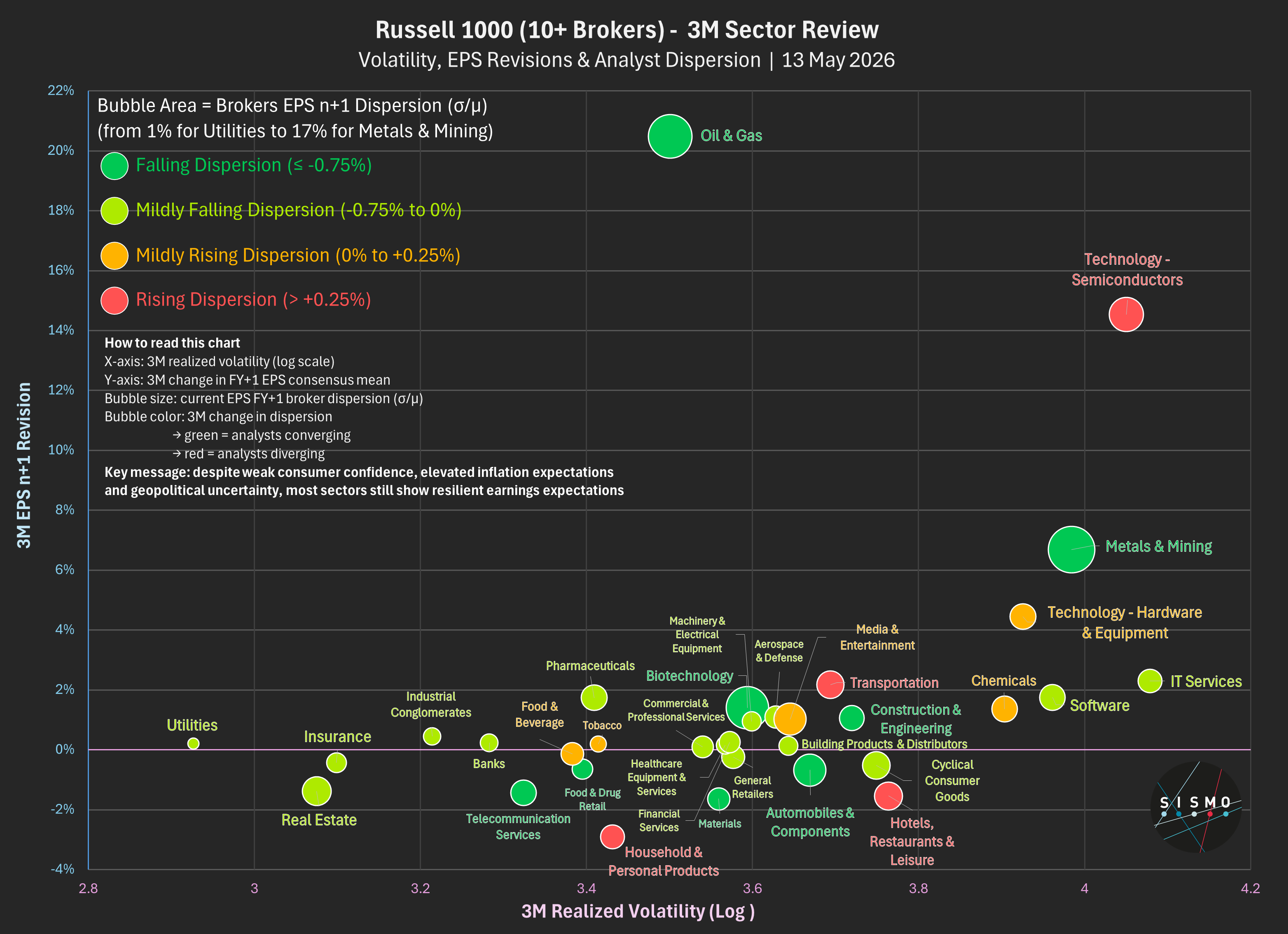

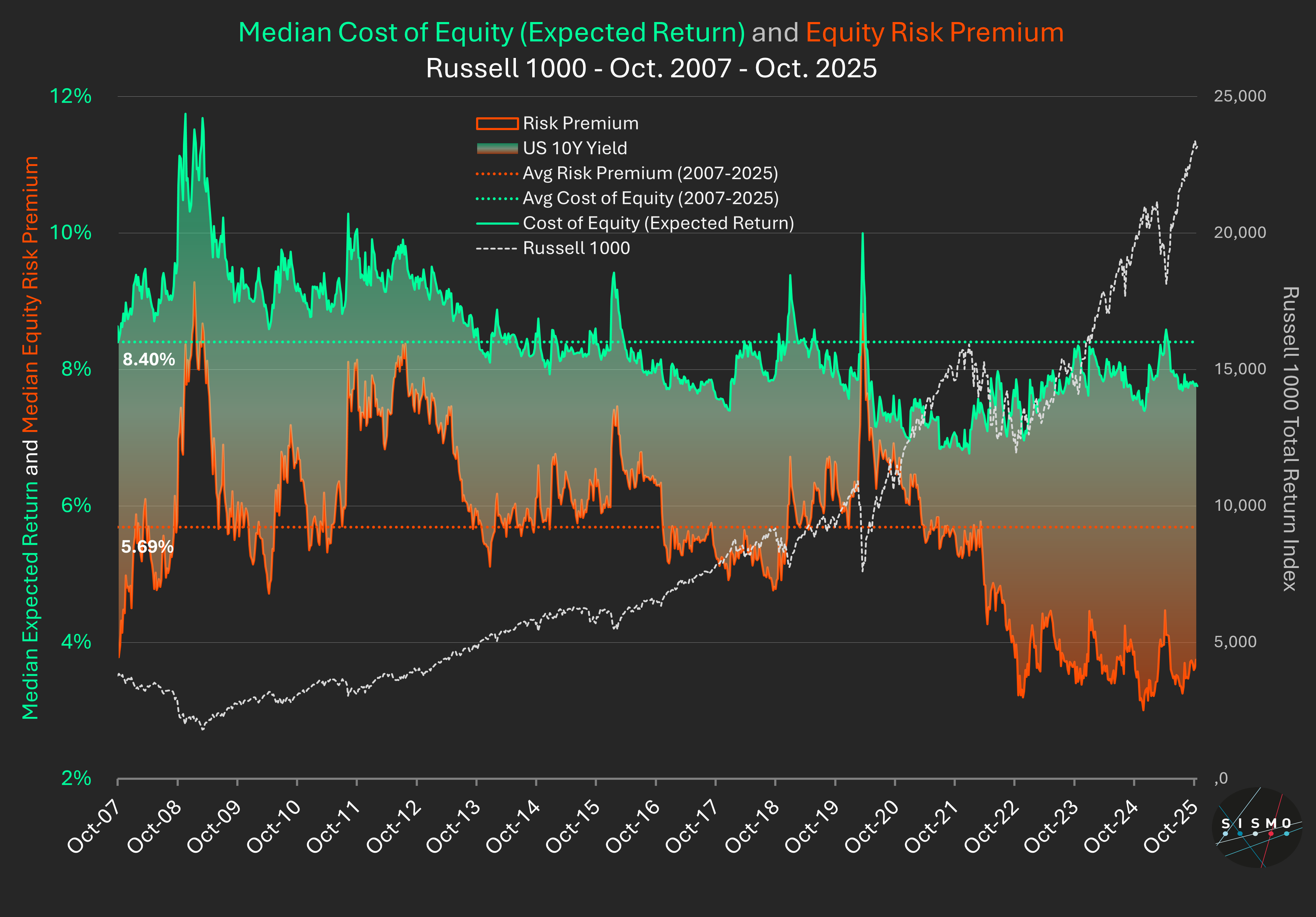

At Sismo, we’ve been tracking the median Cost of Equity for the Russell 1000 since 2007 using a proprietary model applied stock by stock.

Our Cost of Equity combines two price-anchored components:

Today’s reading

What it means

Context and research

Academic work (Fama & French 2002; Duarte & Rosa 2015; Damodaran 2023) defines the Equity Risk Premium as the market’s price of risk - the premium investors demand for holding equities over safe assets. It narrows when optimism rises or bond yields improve.

Estimating expected returns is always model-dependent. Sismo’s framework keeps parameters and data sources consistent since 2007 to ensure comparability over time.

The catch

Our model relies on rolling broker forecasts for the next three years. If these forecasts prove overly optimistic, both the earnings-yield and growth components decline - pushing implied expected returns lower and valuations higher.

Bottom line

We don’t see a bubble yet - but we do see compressed risk premiums and fragile growth assumptions. If analyst visibility holds, markets may hover. If not, gravity will do its work.

For those interested in the academic foundations and methodology behind Sismo’s Cost of Equity and Equity Risk Premium framework, feel free to contact us to explore it in depth.